On January 9th 2007, Steven P. Jobs made the short journey from Cupertino to San Francisco and unleashed a device that would completely disrupt modern commerce. The iPhone.

However, his 90 minute presentation belied three years of battling touch screens, battery life and memory problems. The result? A new era of mobile devices that have been embraced by consumers worldwide.

However, eight years later, most insurers are still struggling to articulate what their mobile strategy is. This is despite the fact that consumers spend almost 3 hours a day on mobile devices and half the world’s population will own a smartphone by 2017. To compound the issue, until recently some insurers argued that mobile is just an extension of the online distribution channel whilst others see some value in its data aggregation capabilities. But few seem to recognise mobile for what it really is; a golden opportunity to re-establish a direct relationship with consumers in an industry that is at risk of complete commoditisation.

Specifically, smartphones and tablets possess unique features that can be deployed to forge a direct and more meaningful relationship with consumers. These features include:

• Click to Call Function

• Tablet Toolkits

• Always On Capability

How these features can be leveraged by insurers will be the focus of this article.

Click to Call Function

The click to call function is a hyperlink embedded in a mobile website or app that initiates a phone call between the user and a particular entity.

| @IBAction func MakeCall(sender: AnyObject) | |

| Click to Call: | var url:NSURL = NSURL(string: “tel://13671591176”)! |

| UIApplication.sharedApplication().openURL(url) |

Specifically, the click to call is particularly applicable to critical illness and life insurance lines due to the complicated and relatively expensive nature of these segments. McKinsey reports that 61% of US consumers researched life and annuity policies.

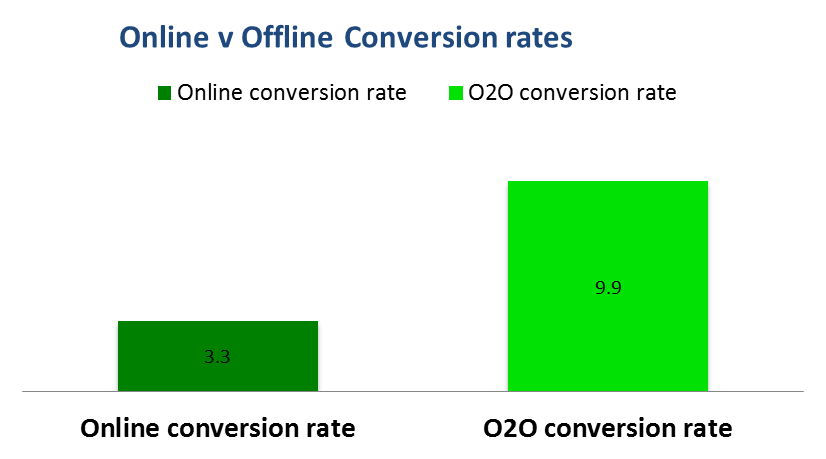

Ultimately, although the click to call function is just a simple line of code, there’s nothing simple about its ability to convert traffic to policy holders. A recent Invoca Analytics report illustrated the impact of click to call on mobile conversion rates.

Furthermore, the potential of click to call has not gone unnoticed by Google who recently included the ability to track the effectiveness of click to call adverts from mobile devices. Specifically, Google claims 70% of mobile searchers have used the click to call function in mobile search results and have rolled out click to call ads in 223 countries that also include metrics such as average call duration, received calls and is reportedly considering the inclusion of call recording functionlity.

Additionally, the emergence of 4G and existing features such as push notifications and geo-location means that the ability to combine the convenience of targeted online services with the reassurance of an offline consultation through the click to call function will only increase.

Ultimately, the click to call function is a great example of a feature that is unique to mobile devices, but more importantly is capable of solving an identifiable pain point in the mobile user journey while increasing conversion rates for insurers.

Tablet Toolkits

The tablet tool kit has already been the subject of much discussion at The-Digital-Insurer. Indeed, the AIA case study explored the tablet toolkit in detail. However, the tablet tool kit is still a leading example of digital insurance on the mobile form factor and so its inclusion here is necessary.

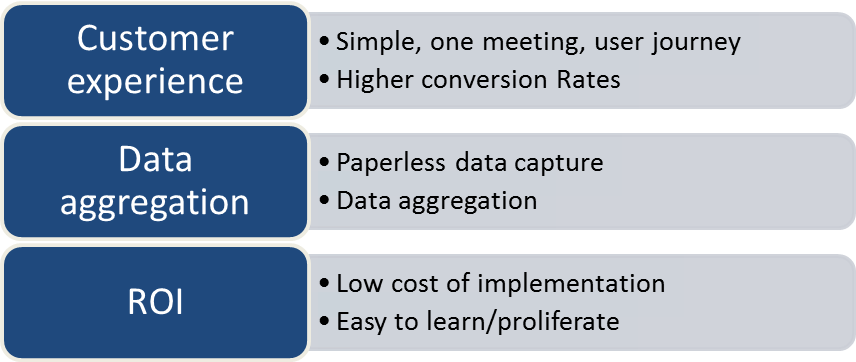

First and foremost, it’s important to note that the tablet toolkit is not just a tactical sales tool for agents. Nor is it a rehash of the bancassurance model. Rather, the tablet toolkit represents a complete over haul of the agency model with three core value propositions.

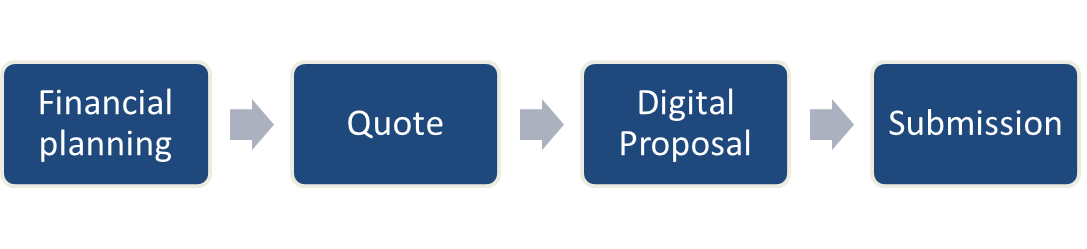

The following user journey demonstrates just how simple this process has become, whilst also enabling the backend data aggregation process.

Tablet Toolkit User Experience:

Ultimately, the potential of the tablet toolkit is far more than just eager speculation. AIA have successfully deployed it in SEA, China and Korea. Specifically, AIA saw an increase in annualized premium per advisor by 34%. Another good example of the tablet toolkit in action can be found in China. In this case, CNinsure (China’s largest broker) launched the CNPad in 2013 and has seen similar success with 63,000 agent downloads of the app toolkit since launch. You can read more about CNinsure’s CNPad in our Snippet.

Always on

The notion of always on is that smart phone users are constantly interacting with their devices and are thus far more engaged with products and services present on smart phones and tablets. Specifically, the engagement rates of mobile devices (fuelled by touch screen internet browsing, push notifications and geo-location functionality). Of all the mobile innovations discussed here, the notion of always on is most open to interpretation. Unlike the click to call function and tablet toolkit, its net contribution to a digital insurer is harder to quantify. However this subjectivity should not be confused for weakness as the sheer engagement levels of mobile apps, mobile browsers and features allow insurers to imbue their value proposition. Additionally, the advent of 4G and exiting features such as push notifications means that mobile users are always within reach. Insurers need to ensure that their products are tailored in such a way that they leverage this always on, anytime/anywhere mentality that consumers are increasingly demanding. Mobile of course, is just one component of this omnichannel approach, but surprisingly its one that many insurers struggle to master.

Daily smartphone usage (minutes):

Conclusion:

“It is not the strongest of species that survives, nor the most intelligent, but the one most responsive to change” – Charles Darwin [1835]

In conclusion, the potential of the mobile channel isn’t just confined to the examples discussed in this article. Other new features and business models brought to life by the mobile revolution include geo-location, targeted advertising through user segmentation and micro-insurance.

For those insurers that are still unsure how to transition to a mobile first world, solace might be found in Facebook’s approach to this new norm. Specifically, Facebook have established an internal mobile bootcamp that teaches the principles of mobile first design, development and deployment whilst devising new monetisation techniques for the mobile channel. This chart from Swiss Re’s Report, “Digital Distribution in Insurance: A quiet revolution?” demonstrates the depth to which the mobile channel is affecting the insurance purchasing cycle.

Ultimately, although traditional distribution channels (agency, bancassurance, telemarketing) will continue to play an important role in the value chain, insurers that ignore the mobile channel do so at their peril. Today’s always on consumers are reaching for the device in their pocket and finding the path of least resistance to researching and purchasing insurance. Insurers who can successfully leverage these features to create seamless user experiences will reap the rewards of a mobile first world.