Ernst & Young published a thoughtful survey and reported it in the last quarter of 2013 as the latest in a series of publications on digital insurance. In this post The Digital Insurer reviews the report and summarises the findings that are of particular interest to insurers in the Asia-Pacific region. Our review is split into 3 sections:

- Main findings

- E&Y view on how insurers should respond

- Digital in Asia – different from the rest of the world?

Main findings from the E&Y survey

[quote align=”center” color=”#999999″]Digital is a catalyst for dramatic change, one that threatens rapid transformation of the competitive landscape and that established

insurers are particularly ill-placed to deal with.

Ernst & Young has summarised their findings from a survey of 100 insurance leaders around the world into 7 areas and this structure has been followed in the review.

1. The need for action is acknowledged by insurers

Nearly 80% of insurers globally acknowledged they are “only playing at” or “still learning” digital insurance and just less than 60% think they do not have operating models that facilitate digital thinking.

2. Are insurers ambitious ahead of their ability to deliver ?

Ernst & Young compared insurers’ aspirations or target future state against current state and found a significant gap – not surprisingly reinforcing the key finding in point 1 above.

However, more surprisingly is the finding that despite this large gap very few insurers were allocating significant financial resources to digital in future plans (less than 10% plan to spend 25% or more in the next 3 years) nor were many engaging in transformation plans (10% of those surveyed) as opposed to a more incremental “business as usual” or “test and pilot” approach.

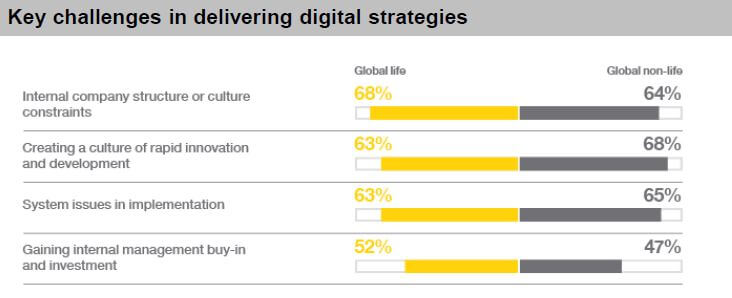

3. Insurers are holding themselves back

Figure 1: challenges to digital transformation are internal

The survey findings identified internal issues as the main challenges that insurers face. Challenges include conservative cultures, organisational structures that prevent rapid change and systems implementation issues (exacerbated by legacy technology).

4. Increasing retention through superior customer experience is the key to success

E&Y’s survey findings in this area built on its previous voice of the customer survey . Key insights are that the top 2 drivers of digital strategies are “enriching the customer experience” (32%) and “regaining more control of customer relationships” (20%). This reflects increasing recognition of the potential to increase engagement with customers and to build longer term relationships using digital capabilities.

5. Distributors need some digital attention as well as customers

The survey correctly identified agents and brokers as both a challenge and an opportunity in digital transformation strategies. The survey findings indicated that the three most significant areas seeing an increase in agents’ use of digital over the next 3 years are:

- Improve efficiency and quality of interaction with customers

- Increase process efficiencies and

- Offer / expose self-service capability to customers

6. It’s also about the data – and the analytics

75% of survey respondents identified analytics capabilities as the most in-demand skill set. Activities such as customer intelligence, segmentation and predictive modelling should be deployed in parallel with other digital initiatives so insurers are learning how to be more pro-active in identifying opportunities and monitoring performance.

7. Insurers need to embrace the mobile and social waves

The survey found that many insurers have not yet fully embraced the consumers’ move to mobile technology and use of social media. A minority of insurers provide quotes and product information via mobile for their customers. Insurers need to invest more and experiment in this area – or risk losing the next generation of insurance customers who are likely to choose their insurers and their insurance intermediaries in a “socially mobile” manner.

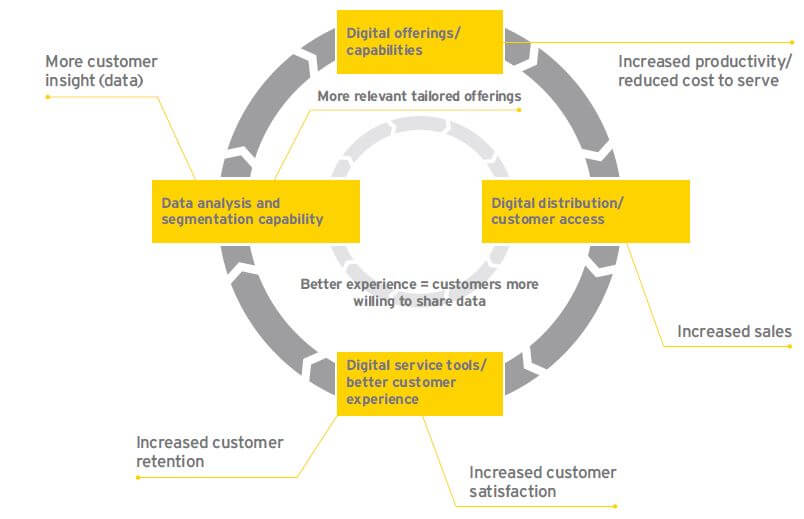

How should insurers respond – E&Y perspective

Figure 2: making the business case for digital insurance – a virtuous circle

Insurers are currently lagging behind the digital curve, and conditions for future success are not yet in place. As a result, many may struggle to deliver on customer expectations; new entrants and digitally leading competitors will look to exploit this failing.

[/quote]The report made a clear call for immediate change by insurers to more aggressively adopt digital insurance. However, the report rightly counsels against a formulaic “one size fits all” approach. The elements to assist immediately are identified as:

- Create a digital strategy with clearly defined ambitions

- Identify initiatives with the most upside

- Share resources to help develop digital capabilities for distribution partners

- Frame the investment argument for digital (and it does require a long-term investment approach – see figure 2)

- Build analytics capabilities in parallel with digital capabilities

- Develop mobile capability and take social media seriously

- Start to embed innovation into organisations

Mid term initiative identified are to shape organisational culture to support collaboration and to move towards cloud computing for improved operational effectiveness.

Digital in Asia – Different from the rest of the world?

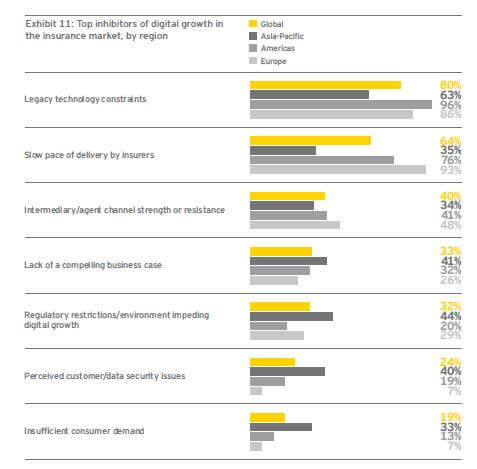

Figure 3: Asia looks different

From an Asia-Pacific perspective, Figure 3 (which is available on page 52) of the report is the most interesting.

At first sight, Asia has the lowest barriers to implementing digital (less legacy technology, relatively fast delivery and less channel resistance are all reported).

So why is Asia-Pacific behind the rest of the world in terms of adopting digital? Especially as we see fast growing markets with young consumers that are leap frogging to smartphones.

When we look at Figure 1 we see that the Asia-Pacific region scored relatively worse than the rest of the world on issues such as “lack of consumer demand”, “lack of a compelling business case”, “perceived security issues” and “regulatory constraints”.

So Asia looks different. Whilst E&Y offered no opinion in its report The Digital Insurer interprets this data as Asia-Pacific being comfortable with the embedded face-to-face insurance paradigm and being slow to realise that other digital models already prevalent outside of Asia will gain significant traction. The Digital Insurer predicts that we are going to see a race in two different directions – incumbent insurers who will start to realise they need to apply digital thinking to transform their agency and bancassurance channels and new entrants (both insurers and non insurers) who are likely to take a ‘digital first’ approach to their business models. Winners will emerge from both directions – but even agency and bancassurance models in Asia will be transformed over the next few years. In fact this race is already on.

The authors of this report should be congratulated for investing in this survey and making a consistent effort to promote digital insurance to a wider audience. Let’s conclude with one final quote from the report:

[quote align=”center” color=”#999999″]Digital levels the playing field, and other consumer industries are keenly aware of this. It’s quite possible that the leading digital insurer of the 21st century has yet to emerge.

[/quote]Further information

All charts and quotes in this review are taken from the E&Y report. To read the original 60 page E&Y Report click this link

This slide share summary produced by the Ernst & Young team is also a useful summary (16 slides):