Digital worksite marketing in Asia : a win-win-win proposition

Worksite marketing is a distribution channel close to my heart. In theory worksite has always offered a classic ” win-win-win” proposition allowing employers to strengthen their bonds with employees, allows employees to buy better products to meet real needs and allows insurers to provide those products in an effective manner. But the reality is that worksite has struggled in Asia. This article will take a look at the worksite model and explore how digital thinking can be used to transform the channel.

Let’s recap: the logic of worksite

The business case for worksite is compelling and is worth restating:

[quote align=”center” color=”#999999″]“Use the workplace and employer endorsement as an opportunity to educate employees on financial needs and to deliver simple and cost effective products to meet those needs”[/quote]The most effective worksite business models will involve all of the following 5 characteristics:

Worksite marketing can deliver good value products to meet identified needs

- Opportunity to educate : Worksite works best when there is an opportunity to educate employees on needs

- A price advantage: Worksite channels offer the opportunity to provide some of the benefits of group pricing to individual purchases. This on top of being an efficient distribution channel

- Product differentiation: Usually in the form of integration with employer provided benefits and by ensuring portability of the employee purchased cover

- Simple products : easy to understand; meeting an easily explained need and easy to purchase

- Builds affinity with the employer : This can be both financial (subsidised purchase or incorporation into a flexible benefits program) and non-financial (e.g. wellness programs, financial education programs, etc)

In short worksite offers an efficient and effective distribution channel to deliver quality products to meet defined needs.

Many professionals have identified the potential of worksite marketing. For example take a look at this McKinsey Quarterly article from 1997 (it is US centric but still relevant to Asia).

So why has worksite struggled over the years in Asia?

With a few notable exceptions, for example AFLAC’s operation in Japan, worksite has not really taken off in Asia to any significant scale. The 5 main reasons for this are:

- HR as the gatekeeper : HR departments assume a moral responsibility to make sure their employees receive professional advice and appropriate products. This creates a significant barrier to the mass adoption of worksite programs, can result in extensive customisation to meet specific needs and give brokers an enormous advantage over insurance providers as the brokers can offer a “best of class” approach to product provision

- Low employee benefit spend : Typical expenditure on employee benefits in Asia is significantly lower than Europe and North America

- Intrusive delivery mechanisms : Worksite marketing typically involves the need for seminars and meetings during office hours and this takes time to schedule as well as making the program reliant on HR department for effective communication

- Complicated and expensive to offer choice (flexible benefits) : Flexible benefits in Asia is a consulting led process that has only been successful with larger organisations (unlike North America there are no tax benefits). However, when flexible benefits have been introduced then worksite opportunities do follow as the need to educate on choice becomes a priority.

- Collecting payments has been difficult : Unlike North American markets payroll deduction is not commonly supported and in some markets electronic giro / direct debit is still not available

What’s changed – why should we take a fresh look at the worksite model ?

Never have I been so excited about a relatively new channel in Asia – and then so frustrated. But is the time right to revisit worksite – is Asia ready for a digital worksite model?

My interest in worksite marketing started in 1997 when I arrived in Hong Kong to work with Guardian Royal Exchange on an innovative worksite marketing and flexible benefits strategy. The 1998 financial crisis put paid to these efforts but ended up launching my entrepreneurial career with an innovative employee benefits start-up in Singapore (which allowed me to keep chasing the worksite dream). I have to declare a deep interest, passion and history for worksite – and I do think, with very strong reasons, that the time is right for this “ugly duckling” to finally shine.

Digital technology, in particular customer centric mobile applications, fundamentally changes the worksite marketing proposition.

For the first time insurance providers are able to provide an engaging technology platform to employees that provide useful services (such as medical claims submission). On the back of employee driven adoption (voluntary opt in) insurance companies are able to establish a digital relationship that can be extended to include the cross-sell of other insurance products.

The most important insight is quite a subtle one: effectively insurance providers are able to change the role of HR from one of gatekeeper to enabler. In Asia, I believe that this will be a relief for many HR departments as they will no longer have the moral responsibility to be seen to vet all worksite related activity and instead can become an enabler for the provision of better financial and health education and solutions. Smart insurance companies will be able to introduce “non-company branded” digital worksite opportunities and then engage HR in discussions for “employer sponsored” upgrades.

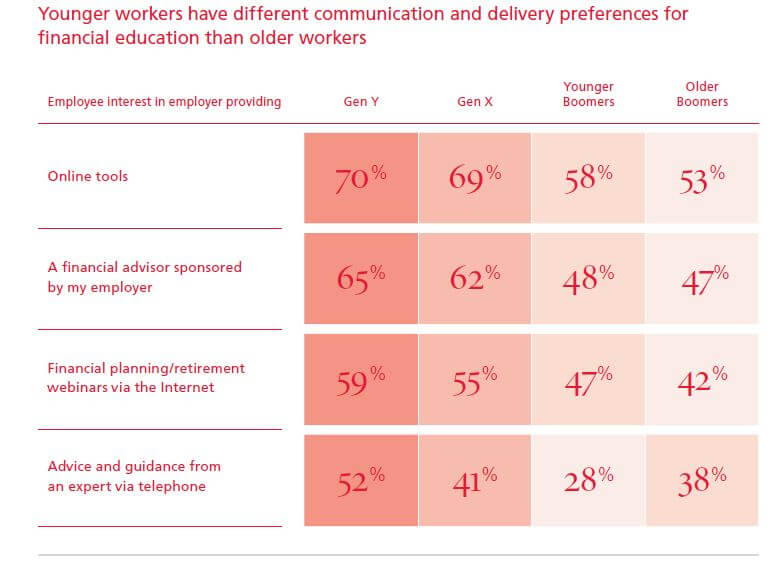

Supporting this approach are significant changes in consumer behaviour when sourcing and executing insurance research and purchases. The table below illustrates the trend to wider adoption of technology (whilst at the same time clearly illustrating that no one single channel of service or sales delivery will dominate i.e. a hybrid approach must be catered for that engages customers on-line, over the phone and face-to-face. The Met Life study reminds me once again how much over the last 10 years the digital revolution is transforming our lives.

Employees preferences for receiving advice and support are diverse – and they increasingly include online delivery of worksite services Source : Met Life Employee benefits trends study

One last set of reasons, not directly related to digital trends, why the time is right for renewed interest in worksite marketing is the continued favourable socio-economic and political trend in Asia. These factors include increases in wealth, aging populations, competitive labour markets and less state provisions of retirement & health services which inexorably increase pressure on both individuals to find solutions and employers to help them to find them (as part of a highly logical employee retention and performance management strategy).

Who can take advantage of the digital worksite opportunity?

The winners of the digital worksite marketing models will be the organisations who are best able to build a complete delivery platform that encompasses the necessary people, process and technological skills. Let’s take a look at who the winners and losers maybe:

- The major brokers: The existing brokers’ mind-sets tends to be driven to offer a highly customised solution to their clients. This approach suits larger clients but is more difficult to create and is not scalable. For the existing brokers to fully take advantage of the digital worksite opportunity they need to access and invest in technology and develop customer service capability to deal with individual employees. They have the advantage of offering “best in class” providers – but can they learn how to operationalise their B2B broking units with a first class B2C service delivery mechanism?

- Insurance companies with significant employee benefits businesses: Strategically these insurers are well placed and finally the unprofitable/ low profit employee benefits businesses can be transformed into consumer orientated businesses. Just look at the valuation difference between an insurance with 500,000 individual life customers and 500,000 employees under employee benefits to get an inkling of the opportunity. Insurers with large employee benefit bases, like brokers, need to learn how to engage with employees and be more consumer centric.

- Insurance companies with sub scale employee benefits businesses: These insurers may struggle to take advantage of the digital worksite opportunity. However, insurers with large agency salesforces could look at digital employee benefits packaged with digital worksite to penetrate small and medium sized businesses directly. Provided this is established as a new channel, with new rules of engagement, it could be a success – and help to provide agency salesforces with a new stream of revenue.

- Banks : The Digital Insurer has coined a phrase “bank-a-site” to represent the opportunity for retail banks. Banks are in the unique opportunity of being able to offer a full range of financial services products which delivered appropriately would be truly engaging for consumers. The opportunity to redefine retail banking and consumer insurance is there for the banks to grab (especially those that can leverage their corporate relationships).

- New entrants: Digital worksite is new and hence there is scope for new entrants. Non-financial services brands, with significant consumer appeal and digital engagement with their clients, will be well placed to provide new offering to employers and their employees. As a market entry strategy digital worksite is likely more attractive than copying existing business models.

My personal view is that the digital worksite opportunity is large enough to support a number of different models but that the fastest route to success is likely to come through partnership between one or more brokers, insurance companies and platform providers. However, those insurers with large “un-brokered” portfolios of employee benefits as well as large agency sales forces have the advantage of incumbency, economies of scale and distribution capability to allow immediate investment in the digital technologies needed that will underpin the new digital worksite business models. Execution against a well thought out road map will most likely characterise those organisations that are successful.

The digital consumer : engagement & content

The successful digital worksite models will also understand that they need to be customer centric. The 4 key strategies to ensure success are:

- A long term digital engagement strategy – probably based around a combination of health and wellness, financial education and rewards programs, i.e education of employees. These programs provide the building blocks for educating employees and developing trust / affinity between all stakeholders

- A ‘digital first’ customer experience capability that delivers superior customer satisfaction through a “digital first” philosophy that also reduces operational costs

- A product purchase mechanism that caters for the hybrid customer – online, over the phone or face-to-face (and even face-to-face will be increasingly digital e.g. using Skype)

- In the longer term the application of sophisticated technology to understand customer on-line activity and to decide on the appropriate follow up activities that will resonate best with the consumer. I would describe this, rather clumsily, as big data analytics generating engagement opportunities that will result in more business being sold. More succinctly it could be called pro-active & intelligence based customer engagement tools. This will allow the right content, product or service to be delivered to the customer in the most appropriate / preferred format.

Future articles will look at some of the implementation challenges of the digital worksite model. This challenge is not just about implementing technology, it involves usability, people, simple products and processes, customer centric, empowering staff to deliver great and immediate service and a large dose of change management that will create the space for a radically different distribution channel to emerge.

Conclusion

I hope I have succeeded in communicating a passion for worksite and have inspired at least a few senior business leaders that now is the time to take a re-look at the worksite opportunity through the lens now offered by digital technologies. The Digital Insurer is actively partnering with insurers, banks, brokers or new entrants who want to innovate and apply digital thinking to create new worksite platforms that can realise the opportunities ahead. Engage with us if you are looking for a partner on your digital worksite journey.

Further Articles

The Digital Insurer is planning further articles to explore the digital worksite marketing model in more detail and to examine the people, processes and technology required for success. We may well look separately at the opportunities for brokers, banks, insurance companies and new entrants.

The Digital Insurer can help

If you need help on using digital thinking to transform your business please get in touch – we are here to help. Please also visit the Q&A area as well as our pages on our Digital Insurance Services.

Share this article – and learn more

Please feel free to share this article with your colleagues. And don’t forget to Sign Up to our email newsletter to be the first to see future articles that are posted on The Digital Insurer.

References and further reading

Please find some references below that have been collated for your ease of reference for further reading on the topic of worksite marketing. They are all useful background reports but were all written before the digital worksite opportunity really opened up off the back of mobile (smartphone / tablet) devices.

Sungard report on worksite marketing 2007

About the Author

Hugh Terry

CEOOther articles

Library: Gallagher – AI, Cyber, Threats and Ethical Hacking

Library: WTW – 2023 Global Report on ESG metrics in Executive Incentive Plans

Library: Aon’s Q4 2023 Global Market Insights Report

Library: McKinsey’s Redefining the future of life insurance and annuities distribution

Library: PwC’s Insurance 2030: Winning moves for group insurers

Library: BCG’s How Insurers Can take on the Climate-Driven Health Crisis

|

Hugh Terry

CEO

EVENTS

Comments