Library: Capgemini and Efma – World Insurance Report 2020

June 2020 featured report:

The digital world is not only catching up with society, it is rapidly overtaking and influencing every aspect of our lives.

Connectivity is no obstacle, but gap with digitally excluded is growing

Most of us readily engage with some form of this intervention/intercession, welcoming the way technology takes the effort out of certain daily tasks.

Which is just as well, as technology is a juggernaut without brakes upon which all social and commercial interactions are increasingly reliant.

So says the Capgemini Research Institute’s World Insurance Report 2020. In addition to coverage of a host of trends the report makes some interesting general points in its introduction. Namely, that:

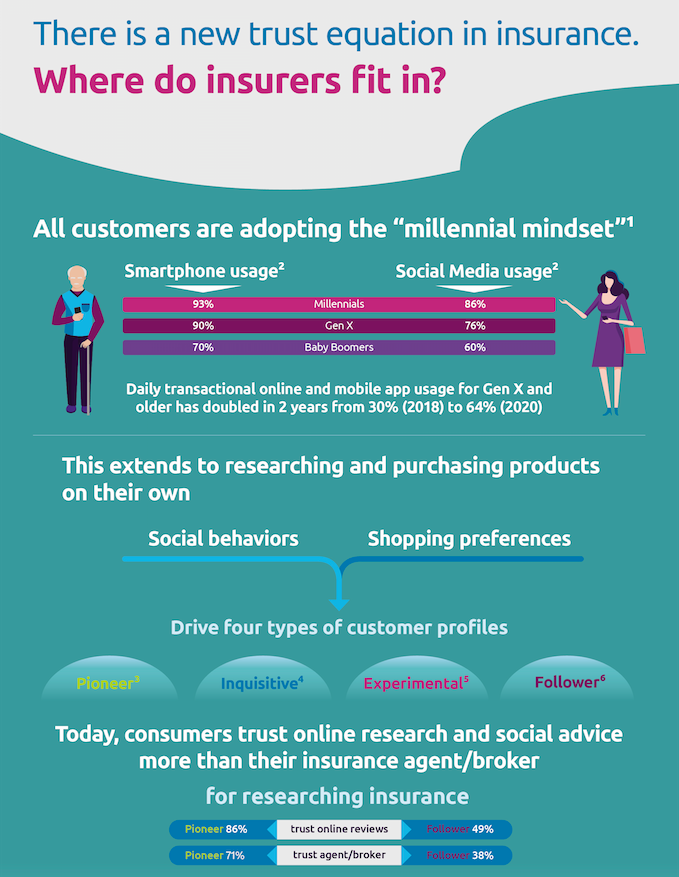

- almost everyone is digital;

- “hyper-personalised”, experience-led engagement is critical; and

- super charged, real time data can be the catalyst to a successful insurer digitalisation programme.

Connecting the world

Digital adoption has grown rapidly in recent years. Even developing markets in Asia have achieved high levels of smartphone adoption, with consumers increasingly seeking digital solutions as a consequence. This adoption of technology is not confined to the young, but crosses all age groups.

The impact of coronavirus has proved beneficial for the process of digitalisation. It has forced new users to adopt digital channels for everyday transactions in order to keep working – or to stay in touch with friends and family.

Purchasing insurance is shaped by the way consumers prefer to do their shopping, but this period has shown social media has become a strong influence.

Customers trust online research and social media testimonials from their friends above broker or agent advice and are more prepared to make independent decisions about buying policies.

These policies don’t have to come from household names – the incumbent insurers that many will have been aware of all their lives. People will buy insurance from non-traditional sources such as tech giants or manufacturers like Tesla.

But it has to be on the consumer’s terms. If an insurer cannot personalise and tailor their customer engagement to provide them with a good experience, they will fail.

The report says that in order to effectively engage with policyholders today, insurers must prioritise:

- Products that meet the changing needs and preferences of the customer through time;

- Communication with customers at the moment they are likely to see insurance as valuable by predicting customers’ needs and offering coverage just when they need it most;

- Digital channels that customers prefer to use, or even enjoy using.

Behind the curve

Yet most insurers are not well prepared for this revolution. Half of the executives surveyed believe product fit is not as important as experience-led engagement. And most firms lack adequate tools and techniques to help them understand and predict when to offer appropriate products

Fewer than a third (<30%) of insurers consider online channels to be effective sales drivers, with more than 60% favouring agent/broker channels.

But if incumbents are not to be left behind, they must embrace the open ecosystem and collaborate with mature insurtech firms and third party specialists if they are to develop innovative solutions that consumers actually want to use.

Exploiting real time data can give a major boost to an insurer’s digital project. This data provides invaluable detail providing insurers with actionable insights into what policyholders want and how they might be willing to engage.

This allows insurers can assess their portfolios to determine whether their products are meeting their customers’ immediate needs and allow them to assess the right time to offer enhancements or promotions.

High demand for on demand cover

The COVID-19 lockdown has caused many to consider their relationship with their current insurers. In the APAC region, there was increased engagement and an awareness of the protection it offered policyholders.

In other regions, such as the UK and US, there has been unhappiness about the way the insurance industry dealt with the crisis.

With the ability to travel limited by government mandates, auto insurers in the US and UK offered partial rebates to customers for the period they were unable to use their cars.

In the UK, weekday car journeys fell by 60% in the month between lockdown and the middle of April, according to data from motoring organisation, The AA.

The same research found among that 22% of 20,000 UK drivers will drive less than they did before the crisis.

But one insurtech startup saw its business boom during lockdown. By Miles is the first to offer a pay-per-mile insurance product in the UK, which only charges customers for what they use, plus an upfront cost for when the vehicle is parked.

“This crisis has shown UK drivers what we’ve known for a while: the way car insurance works now isn’t working for everyone,” says James Blackham, co-founder and CEO of By Miles.

“They’re rightly questioning why they should pay for insurance they’re not able to use, and asking why traditional car insurers can’t provide a flexible alternative to meet their needs.”

Usage based cover is far more flexible and costs less than a traditional policy. Since its launch in July 2018, By Miles has already sold nearly 20,000 policies. But its strongest ever sales week was in April.

The UK has 19 million low mileage drivers covering less than 7,000 miles a year.

Insurers must promote digital inclusion

The report raises another important subject that is not contained in most reports on the insurance industry’s digitalisation project.

Although most people have gone digital, the lockdown has identified a growing gap between the world’s online and offline populations.

The authors say that the need to address “digital exclusion” must not be left to insurers, or NGOs, but that public and private organisations “must come together to ensure that access to essential services isn’t denied to the digitally marginalised”.

The findings are summarised in another Capgemini report, “The Great Digital Divide: Why bringing the digitally excluded online should be a global priority” which shows that before the pandemic, more than two thirds (69%) of those without online access were living in poverty and that 48% of that group wanted access to the internet.

This division has intensified across the globe due to effects of the COVID-19 crisis.

More than a third (40%) of offline people living in poverty have not used the internet because it costs too much. But the age group most marginalised is not the elderly, but those between 18 and 36 years old (43%).

COVID-19 has changed the way people live, work and socialise. In some cases, these changes are permanent and as unemployment increases, digital inclusion is almost essential to prevent people become isolated within their communities.

Building bigger and better customer bases

Social interaction is only a small part of the story. Almost half (44%) of offline respondents said finding better jobs and education would be easier if they had access to the internet.

Overall, 29% wished they could search and apply for jobs online. Among those aged 22 to 36, this increases to 41%.

This is not altruism. It makes good business sense. This digital empowerment will swell the ranks of consumers that insurers target. But the responsibility of bridging this digital gap must be shared between the public and private sector.

Organisations are increasingly being asked to demonstrate their value to society, not only shareholders. Digital inclusion and equality should be integrated into business strategies, say the authors.

While the private sector seeks to increase inclusion, governments must lead the way in providing internet access and availability, particularly among marginalised communities.

“In the wake of this pandemic, we expect to see a closing of the digital gap – for example, elderly people who have previously not felt a need for digital access will quickly find themselves engaging with digital tools in place of face-to-face socialising and the provision of goods,” says Lucie Taurines, global head of digital inclusion at Capgemini. “However, this is reserved for those who can get access to the internet but have previously chosen not to. The impact will be felt among those who still can’t use online services, whether through a prohibitively high cost or a lack of local provision. Here we’ll see a polarising effect, especially for those already living in or falling under the poverty line.”

Insurance will retain the human touch

Last month’s featured report looked at how COVID-19 had led to a new appreciation among consumers in some APAC markets for their insurance cover.

Many said they would give up dining out, gym memberships and even auto insurance before they considered cutting their life cover. While this was an interesting – and welcome – development, not everything is going to be changed by the pandemic or digitalisation. Technology may be seen to be replacing the human face of insurance, but that couldn’t be further from the truth.

Innovations in artificial intelligence (AI) and machine learning (ML) are beginning to automate mundane and repetitive tasks, releasing the human capital resource – or real flesh and blood employees – to focus on dealing with non-standard, or complex situations and thereby improve and personalise the consumer’s experience of dealing with the insurer.

You may remember earlier, that 60% of the executives surveyed preferred agency and broker channels to digital ones. And with good reason. Insurance is a people business and some consumers prefer human interaction at certain times.

Just as insurers are using technology to augment certain operations, so too is this being applied to the agency channel.

Ping An’s huge investment in AI is not designed to replace agents, but expand their ranks to one million and to make them the best trained, most efficient and carefully governed as possible.

This doesn’t mean an agent will be limited by the insurer’s augmentation, but liberated by its use.

Agency Height, a publication for US insurance agents believes that integrating technology is essential to success. However, it doesn’t replace good, old-fashioned networking and relationship building.

Yes, agents will rely more heavily on technology to generate leads, process policies and manage customer interaction. But the power of social media, and in particular referrals from friends and family, will be more important than ever before.

The future of insurance

The future is not only based on technology, but relies on it. We know this to be true, even though many insurers have yet to start their digitalisation project in earnest.

What we must also remember that despite the industry seeing a ‘rise of the machines’, the insurer of the second half of the 21st century will still be a people business, helping consumers cover their risk and being there for them when things go wrong.

But it is only the ones who succeed in fully integrating seamless operational reforms that support and augment their workforces that are going to benefit from the ongoing revolution.

Link to Full Article:: click here

Link to Source:: click here

About the Author

Pádraig Floyd

Research EditorOther articles

Library: Gallagher – AI, Cyber, Threats and Ethical Hacking

Library: WTW – 2023 Global Report on ESG metrics in Executive Incentive Plans

Library: Aon’s Q4 2023 Global Market Insights Report

Library: McKinsey’s Redefining the future of life insurance and annuities distribution

Library: PwC’s Insurance 2030: Winning moves for group insurers

Library: BCG’s How Insurers Can take on the Climate-Driven Health Crisis

|

Pádraig Floyd

Research Editor

EVENTS